Parent borrowers have been shut out of Biden administration’s recent student loan relief measures, but this loophole could help

- Parents who took out federal loans on behalf of their children are ineligible for the Biden administration's new student loan relief measures, including the Saving on a Valuable Education repayment plan.

- Thanks to a "super-secret double consolidation method," there is a way for parent PLUS borrowers to access SAVE.

- However, borrowers who want to pursue this option must act quickly. The U.S. Department of Education is expected to close this loophole by July 2025.

After the Supreme Court rejected President Joe Biden's sweeping forgiveness plan earlier this year, the president announced a series of other relief measures for student loan borrowers.

Already, Biden has managed to erase $127 billion in education debt for more than 3.5 million borrowers, largely through Public Service Loan Forgiveness and income-driven repayment plans.

Get top local stories in Connecticut delivered to you every morning. Sign up for NBC Connecticut's News Headlines newsletter.

The most beneficial so far has been the new Saving on a Valuable Education repayment plan, which aims to get federal student loan borrowers the lowest monthly payment possible — even $0.

More from Personal Finance:

62% of Americans live paycheck to paycheck

Why working longer is a bad retirement plan

Credit scores hit all-time high even as overall debt rises

"It's almost like a grant after the fact," said higher education expert Mark Kantrowitz.

Money Report

Yet, parents who took out loans on behalf of their children are ineligible for all income-driven repayment plans, including SAVE.

"Many of these provisions do not apply to parent borrowers," said Kalman Chany, a financial aid consultant and author of "Paying for College" from The Princeton Review. "They're out of luck."

Once families hit their federal student loan limits, they often turn to federal Parent PLUS loans to secure the financing they need to send their children off to college.

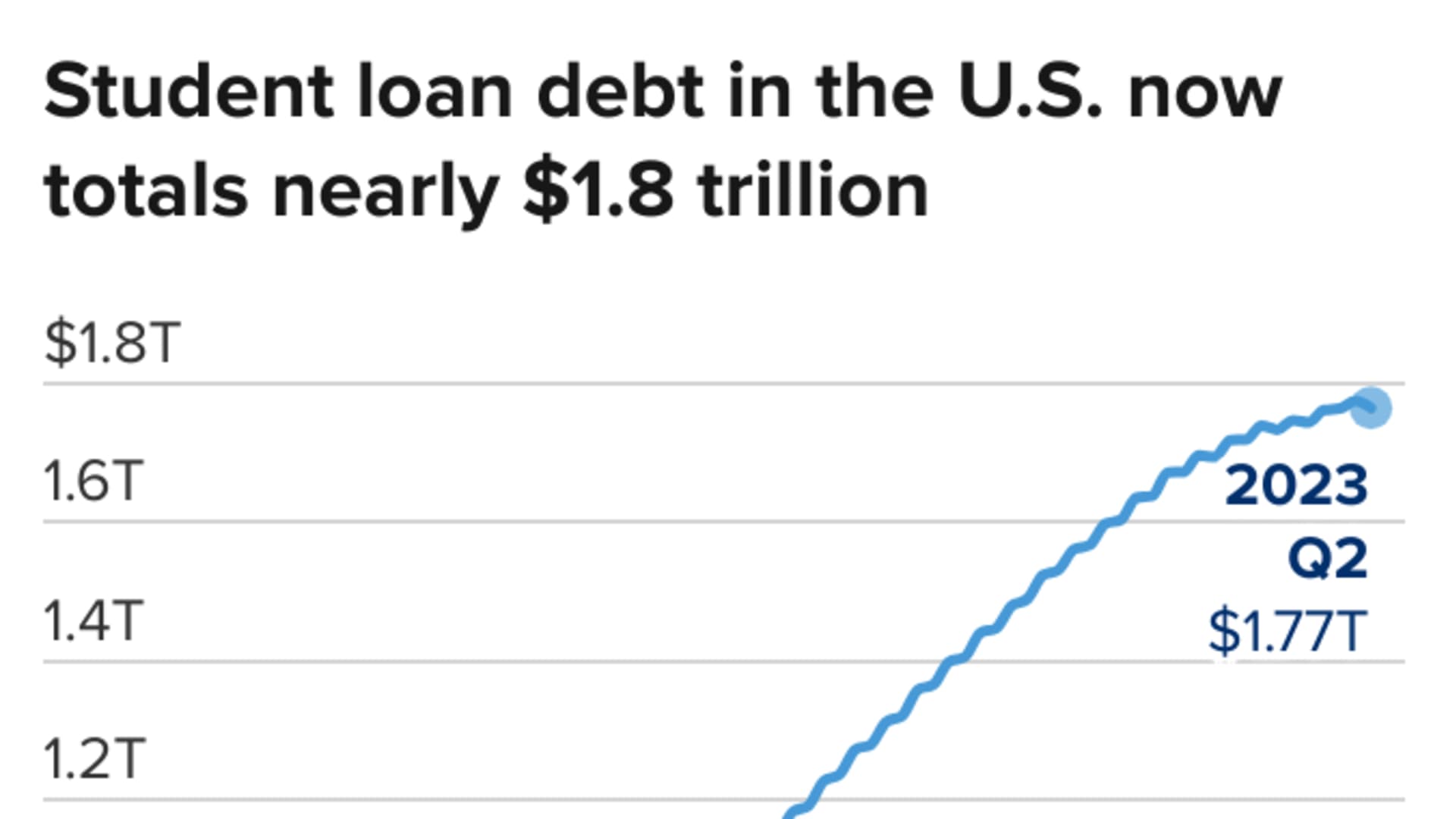

As college costs rose, so have student loan balances, plus the share of debt owed not just by graduates, but their parents, as well.

Parent PLUS loans account for $111 billion

The share of parents taking out Parent PLUS loans to help cover the costs of their children's college education has increased steadily over time, research shows, almost quadrupling over the past two decades, according to Kantrowitz.

Currently, 3.7 million parents have $111.3 billion in Parent PLUS loans outstanding. The average parent PLUS loan is roughly $30,000.

Parent PLUS loans also come with an interest rate of more than 8%, compared with 5.5% for undergraduate student loans.

There could be help for parents after all

The only option for parent borrowers outside of the standard, graduated and extended repayment plans is a "special limited window of opportunity" to consolidate Parent PLUS loans into direct consolidation loans, making them eligible for income-driven repayment plans, Chany said. However, this process "is complicated."

The Institute of Student Loan Advisors provides step-by-step guidance on this loophole — referred to as the "super-secret double consolidation method" — which enables parents to gain access to lower-cost income-driven plans.

"The gist is that if you consolidate a consolidation loan, and are careful about how you go about doing it, that new loan will be eligible," Kantrowitz explained. This also entails switching to a different loan servicer and submitting a paper form, among other steps, so the new loan is no longer tied to the original Parent PLUS.

Still, the extra legwork is worthwhile. By switching from income-contingent repayment to SAVE, for example, payments on undergraduate loans could be reduced from 20% of discretionary income to 5%. "It cuts the payment potentially by a factor of four," Kantrowitz said. "It is a dramatic difference in the monthly loan payments."

The savings over 20 years could amount to "thousands or even tens of thousands of dollars," he estimated.

But "there is limited time left to take advantage of it," Kantrowitz also added. The U.S. Department of Education said it will close this loophole after July 1, 2025.

Subscribe to CNBC on YouTube.

Don't miss these stories from CNBC PRO:

- 75% of Warren Buffett's equity portfolio is in just 5 stocks. Here's what they are

- These two banks just hiked their 1-year CD yield to 5.3%

- A prudent way to bet on a bounce in Apple following its post-earnings decline

- Stifel says the S&P 500 will keep climbing 'wall of worry' to hit 4,400, gives 10 stocks to play rally